The “key currencies” bear the usual risks faced by bankers. No bank could return deposits in banknotes to its clients if all of them demanded withdrawal at the same time. The acceptance of deposits and their mobilization through checks make “bank money” the real money. Despite the technical and political difficulties that may arise, the dollar and the pound will continue to be reserve currencies and means of international payment if, once the gold reserves of the United States and Great Britain are exhausted, the rest of the world continues to accept these currencies as a means of payment. Conversely, if this acceptance were to cease abruptly and universally (a hypothesis as unlikely as the previous one), despite the existence of sufficient gold reserves for full conversion into precious metal, these two currencies would immediately lose their international character.

In any case, the problem arises in its full magnitude on the day when the two countries mentioned decide, in order to regain their financial independence, to voluntarily convert the dangerous liability represented by their monetary “balances.”

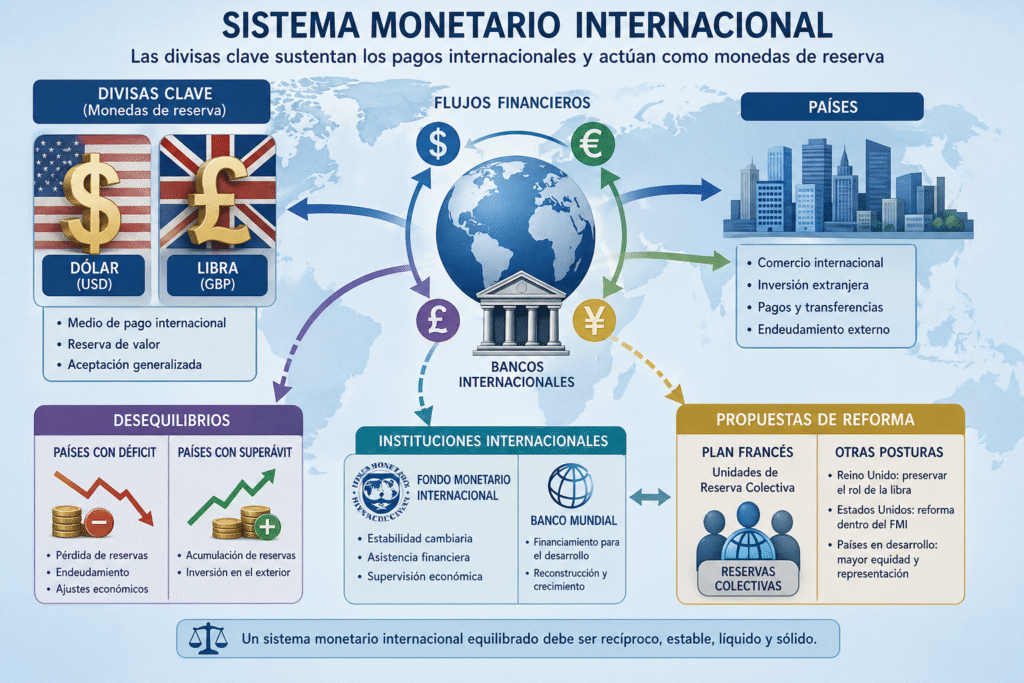

This massive conversion would mean, if it takes place, the end of the long-standing international role of London and the end of the international role that the dollar gained in 1914. Such abandonment would grant greater freedom to the domestic economic policy of the countries concerned, but history has shown how strongly the international role of these two currencies has been defended. It can be assumed that this abandonment will never be voluntary; London has managed to defend the international role of the pound, not only in 1925 but also more recently, against the E.P.U. Moreover, this situation also entails certain advantages that Giscard d’Estaing highlighted. Key currencies are dominant and, therefore, burdensome for those that are not. In a lecture delivered at the Faculty of Law in Paris on February 11, 1965, the French Minister of Finance defined four criteria that allow the value of a sound international monetary system to be assessed:

- Serve the mutual interests of participating countries;

- Lead countries to restore balance in their balance of payments when it is disrupted;

- Provide the world with sufficient liquidity to meet the needs of global expansion;

- Be a stable system.

Regarding the first point, it can be said that the current system does not offer conditions of reciprocity; “It concentrates all the burdens, it is true, but also all the advantages on the countries issuing reserve currency.” When a country without a privileged currency faces a deficit vis-à-vis the rest of the world, it is forced to use its gold and foreign exchange reserves or to incur debt by resorting to international credit. By contrast, a country whose currency is used in international payments can finance its deficit by paying in its own currency. As for the second point, the system is not capable of encouraging countries with key currencies to restore balance in their balance of payments, since they can indefinitely finance their deficit with their own currency. It thus appears as if the United States had exported its inflation. The underlying analysis is not inaccurate, but it overlooks a reality that is infinitely more complex. Finally, the French Minister of Finance considers that the international monetary system is not stable:

“We are faced with a paradoxical situation in which the dollar, as a world currency, continues to be a strong currency, while the dollar, as a reserve currency, is increasingly less desired by the states that hold it.”

In this very expression there is more than a paradox; there is a contradiction. A strong currency due to the economic power of the United States, the dollar is increasingly less sought after as its effective convertibility into gold appears more and more uncertain. Under these conditions, the international monetary system must be reformed so that it can meet the four fundamental criteria defined by the French Minister of Finance. Unfortunately, there is such an “inflation” of reform plans that it becomes difficult to distinguish the fundamental principles that either complement or oppose one another. The French plan and the plan presented by Great Britain are radically opposed: one aims to reduce the importance of key currencies, while the other seeks to preserve the international role of the pound. The United States does not officially present any specific plan. However, it calls for any reform to be carried out within the framework of the I.M.F., where its influence is institutionally predominant. France insists on the need for the United States to rebalance its balance of payments; the American Secretary of the Treasury responds by emphasizing the importance of surplus countries adjusting their position in the same way as those with deficits. National interest guides, on all sides, the search for new systems.